Preparing for BID - What is most important for you?

Updated

by

Caroline Pollard

Updated

by

Caroline Pollard

This week we look at the 'What is most important for you?' section in Chief to help prepare you for the introduction of Best Interests Duty (BID) on 1 January 2021.

As part of your Responsible Lending obligations (under RG 209.43), you must make reasonable inquiries about your client's financial situation, requirements and objectives. Although the Responsible Lending obligations and BID are distinct obligations (as stated in RG 273.23), the information gathered for the purpose of Responsible Lending may help you to determine what is in your client's best interests.

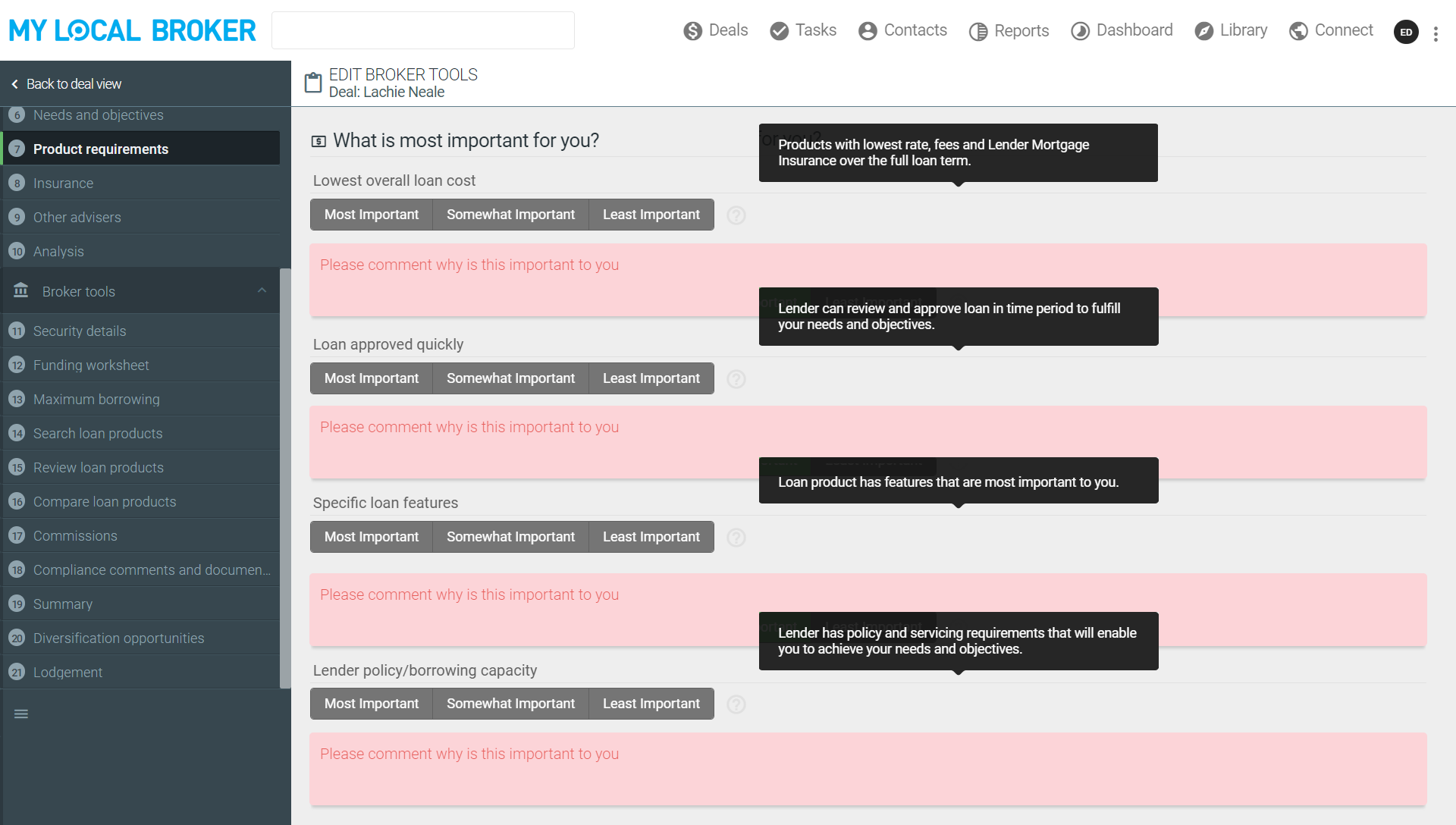

What is most important for you?

In order to make your recommendation, you must complete the following categories in the 'What is most important for you?' section (as per RG 273.48):

· Lowest overall loan cost

· Loan approved quickly

· Specific loan features

· Lender policy/borrowing capacity

This will be determined by what is most important to the client. These need to be completed in order of importance to the client and only one category can be marked as the 'most important'.

Further commentary is required when a category is marked as 'most important'. e.g. the client's most important priority is to secure the purchase of their new principal place of residence within 21 days and requires their 'loan approved quickly'.

What's changing in Chief?

Chief has already been enhanced throughout 2020 in preparation for BID, with the completion of the above 'What is most important for you?' section in the 'Product requirements' tab to be made mandatory this month.

As per RG 273.45, in order to meet the BID you will need to understand your client's needs, goals and financial situation. The information captured within the 'Product requirements' tab will continue to populate information into the 'Credit Proposal & Preliminary Assessment', supporting your recommendation. Further enhancements in Chief will ensure that the disclosure documents represent the full assessment that has been made into what is most important for your client and will provide more clarity on the reason for lender and product selection.

It is also important that all information provided is accurate and complete. RG 273.42 states that a Mortgage Broker who provides incomplete or inaccurate information will fail their BID obligations, even if the inaccurate information would increase the likelihood of approval or give your client access to better terms.